Semiconductor in numbers: Renewable gains outpace grid realities

Share this insight

Regional constraints shape renewable adoption

Across semiconductor manufacturers’ global operations, renewable energy progress remains uneven. While 100% renewable electricity use has been achieved in some regions, many of the largest fabs are located in markets where supply is constrained, demand is rising rapidly, and procurement frameworks are less accessible.

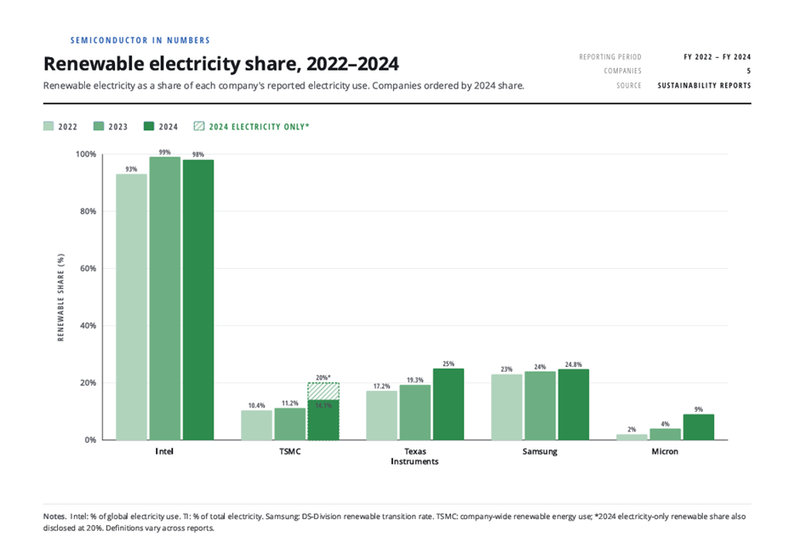

Intel reports significantly higher renewable electricity penetration than peers, reaching approximately 98% globally in 2024. The company’s geographic footprint has been a key advantage, with a significant share of operations in the United States and Europe, where renewable markets are more mature and procurement mechanisms more accessible. This contrasts with peers whose manufacturing is more concentrated in Taiwan and South Korea.

In Taiwan and South Korea, renewable deployment remains constrained by limited build-out, strong industrial demand, and power markets historically dominated by state utilities, which restrict corporate access to renewable procurement mechanisms. While capacity is expanding, policy, pricing, and market design continue to limit the ability of large industrial users to scale renewable electricity use at pace.

This is reflected in manufacturers’ global renewable shares. Micron achieved 100% renewable electricity for its mainland China and Malaysia operations by 2024 and is targeting full coverage in the U.S. by 2025, yet its global share remains around 9%, reflecting reliance on more carbon-intensive grids in key production locations such as Taiwan and Singapore. Samsung’s Device Solutions division is similar, with a global share of around 25% despite reaching 100% in the U.S. and China, largely due to limited renewable availability in Korea. TSMC follows the same trajectory, with overseas subsidiaries at 100% but a global share of roughly 20% due to low uptake in Taiwan.

Role of market-based procurement mechanisms

Much of the sector’s reported progress is enabled by market-based procurement mechanisms, which allow companies to scale renewable electricity use beyond what local grids can supply.

Intel exemplifies this approach. Since beginning renewable procurement in 2003, the company has built a diversified portfolio spanning on-site generation, power purchase agreements (PPAs), and energy attribute certificates (EACs), enabling it to match electricity consumption with renewable supply across markets rather than relying solely on local grid decarbonisation.

However, these mechanisms differ in their impact on physical electricity supply. Intel’s on-site capacity - around 50 MW globally, meets only a small share of demand, with the majority of its reported 98% renewable share derived from PPAs and EACs. As a result, this figure reflects contractual sourcing rather than the electricity physically consumed at each site.

Peers follow similar approaches. Micron generated around 270 MWh on-site in 2024, compared with more than 780,000 MWh sourced through PPAs, green tariffs and RECs, while Texas Instruments includes both on-site generation and retired RECs in its accounting. While aligned with GHG Protocol standards, these methods do not necessarily reflect real-time grid supply.

Closing the gap between reported and physical supply

These dynamics point to a persistent gap between reported renewable electricity use and the underlying energy mix. On-site generation remains negligible relative to demand, leaving companies heavily dependent on external procurement to scale renewable electricity use.

At the same time, renewable deployment is weakest in the industry’s most important manufacturing regions, where energy-intensive production is concentrated and grid decarbonisation remains slow.

However, this gap reflects a transitional phase. As renewable capacity expands, markets mature, and grid infrastructure improves in key manufacturing regions, the alignment between reported and physical renewable electricity use is expected to strengthen. In the meantime, current procurement strategies are already helping to scale renewable markets and support longer-term system change.