Chart of the month: February 2023

Share this insight

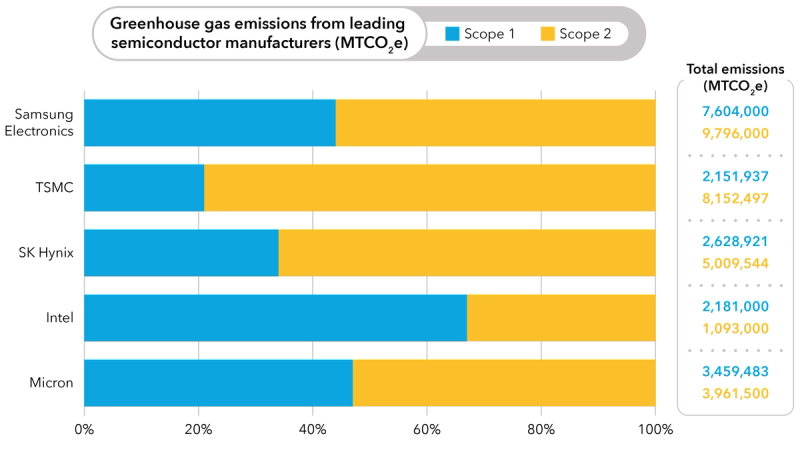

Source: Company reports.

This month’s chart demonstrates the distribution of greenhouse gas (GHG) emissions between scope 1 (direct) and 2 (indirect) as detailed in the sustainability reports of the top five manufacturers by GHG emissions. The scope 2 figures used reflect emissions produced by the manufacturer through use of heat, energy and cooling while acknowledging the inclusion of purchased renewable energy.

Extrapolating from research completed by McKinsey & Co regarding semiconductor fab emissions, the industry standard proportions of scope 1 versus scope 2 emissions are approximately 45% and 55% respectively (omitting scope 3 emissions). Samsung Electronics and Micron reflect this average most closely, while TSMC and SK Hynix have a higher proportion of scope 2 emissions, and Intel demonstrates a much higher proportion of scope 1 emissions.

The most prevalent source of direct (scope 1) emissions at semiconductor manufacturing companies are process gases which have a high global-warming-potential (GWP) such as perfluoro compounds (PFCs). These greenhouse gases are integral to the manufacturing process and are therefore hard to abate, but semiconductor companies are beginning to find less harmful alternatives. For example, Samsung Electronics has replaced C4F8 with G1 in some processes, while Micron plans to invent new lower GWP dry etch chemistries. In fact, the sustainability reports published by all five companies make explicit reference to substituting harmful gases or chemicals where possible as part of their strategies to reduce scope 1 emissions.

The high energy requirements of semiconductor manufacturing means that scope 2 emissions (indirect emissions resulting from energy and heat usage) are generally higher than scope 1 in this industry. Intel’s low proportion of scope 2 emissions highlights the important role of renewable energy in mitigating scope 2 emissions, as Intel achieved 80% renewable energy globally in 2021. Intel is prioritizing a faster transition to renewable energy than other manufacturers.

Indirect emissions from the value chain (scope 3) have thus far received less attention. Some companies neglected to disclose them in their sustainability reports, likely because they are hard to track and mitigate. However, other semiconductor manufacturers are seeking to control these emissions by requiring that suppliers take steps to disclose or mitigate their GHG emissions. TSMC requests that suppliers set targets for emissions reduction, whilst SK Hynix intends for all suppliers to complete ESG self-assessments.

Despite these measures, and a growing focus on sustainable practices in semiconductor manufacturing, striking the balance between innovation and sustainability will prove difficult. Semiconductor manufacturing is a notoriously energy and resource-intensive industry; four of the five companies on this chart reported increased emissions of some kind for the year 2021 due to increasing production and complexity in the manufacturing process.

In order to reach sustainability goals, semiconductor manufacturers will have to collaborate to foster a mutual approach to both targets and metrics for GHG emissions. Semiconductor manufacturers must find innovative ways to advance technology while halting, or at least slowing, climate change.

Share this insight