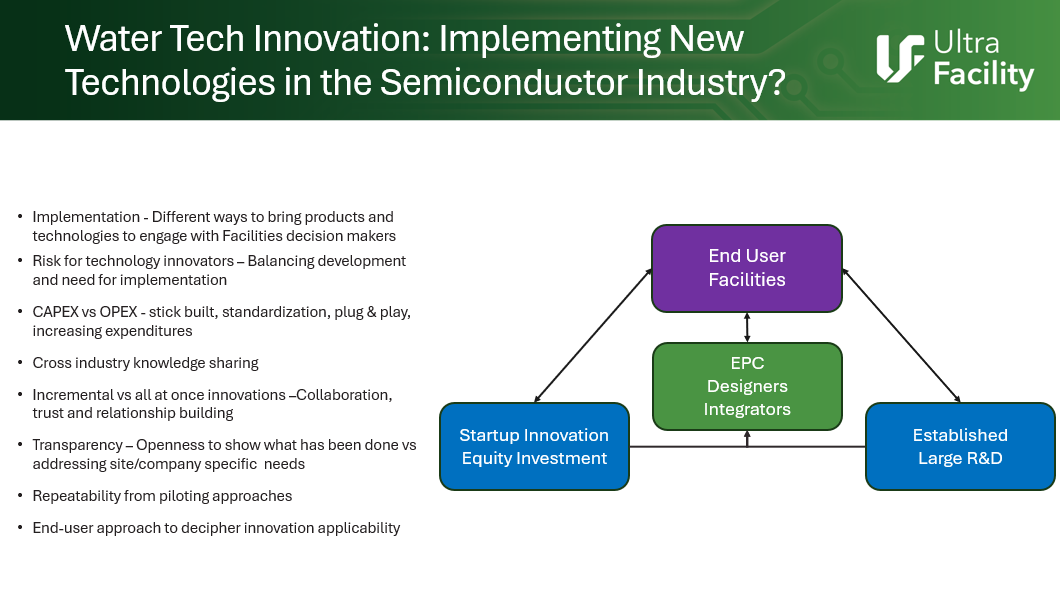

Water-as-a-service: The Next Tool for Scaling Semiconductor Fabs

Share this insight

Lydia Whyatt is a water consultant with 20 years' experience investing in water technology and infrastructure. Serving as managing director of Eau/Zero, Whyatt advises business and finance leaders on water management. After advising on a water-as-a service (WaaS) project between Veolia and a major semiconductor manufacturer, she provided Ultrafacility with insights on how the service model can help address some of the water challenges faced by semiconductor manufacturers.

What is driving the adoption of WaaS in the semiconductor industry?

There is a significant shortage of trained operators. At the 2024 UltraFacility conference, every major semiconductor facility leader emphasised the desperate need for young talent in water treatment roles. Training for sophisticated systems like UPW and wastewater is challenging. While in-house expertise for ultrapure water is vital is because it is part of the manufacturing process, wastewater reuse is less connected to manufacturing process. As such, manufacturers are more likely to turn to third parties for expertise. To sum up, complexity of treatment and lack of expertise are driving water-as-a-service.

Do you anticipate more growth in the future, what would drive this?

Outsourcing is not something the semiconductor industry has traditionally considered, but fabs are adapting. Reshoring manufacturing to the US and Europe as a result of geopolitical risk is creating demand. These new plants don’t have expertise in water, so that drives water-as-a-service, and for locations like Arizona, water shortages are obviously also a driver.

Another emerging driver is that water use is so high, that even if a utility is willing to supply water and take it away for a cost, they are limited by their own infrastructure. By the times fabs have treated the water to a dischargeable level, particularly incoming concern over PFAS, they may as well reuse it, and for that they need expertise, so it also drives outsourcing.

How does outsourcing water treatment influence operational risk?

It is a double edge sword. The positive side is that you have experts in the water industry, so you aren’t just relying on internal expertise. If something happens at the plant, you have large water operators supporting you while you fix the problem, rather than doing it all yourself.

The negative, particularly for the semiconductor industry, is control, which is particularly important for UPW where there is larger potential for manufacturing losses and therefore sizeable expenses. None of the water operators are willing to take on consequential damages. If they have not delivered the plant properly, they will take responsibility for that, but only to the level of what they are being paid, not to the level of consequential damages. This is the key concern for semiconductor manufacturers: they will not be compensated if something happens to their plant.

So, on one hand you are mitigating the risk of the plant not working properly, on the other hand you need to manage the risk that your plant or manufacturing is affected by an external party.

How does the cost of water as a service compare to owning a treatment plant?

The negative side is it is a bit more expensive than having your own plant, as the service provider would need to have a margin on their labour. However, we are talking 10-20% margin, max 25%. So, it is not a killer and for the amount of risk you are outsourcing, that is the balance you need to strike for yourself. The positive is that you can rely on an experienced operator who can support you through a problem if it does appear.

Has there been any other specific challenges you have seen when implementing the water-as-a-service model?

Trust is probably the key issue between the client and the operator. You are hiring somebody for a long time. The client could add materials to the water not realising it will create havoc on the biological treatment, then they may not want to tell the operators what they have done because it will cost them money when the operator needs to reboot the plant.

That relationship needs to be very well managed. If the client is honest and communicative, the operator is generally more honest in terms problems and potential solutions. That is the key to success.

What are the key considerations for fabs when deciding between WaaS versus traditional water management approaches?

Do they have the internal expertise, or would they prefer to rely on external resources, and are they willing to pay for it? If they do not want to incur that cost and are confident in their operating plan, they would most likely be inclined not to outsource. However, if they are undertaking something new, are not confident in the process, and there is no alternative destination for the wastewater, then outsourcing could be a suitable option.

On a wider industry level, what else can be done to build that trust and make WaaS more attractive?

Particularly for semiconductors, you need to choose the right party. Often, there is an existing relationship with the water solutions provider, not on a service basis but perhaps on equipment. If the supplier has solved problems for you in the past, then the trust is there. Additionally, larger groups tend to win those projects because the client relies on the operators being available 24/7. That is a key criterion, if the suppliers don’t respond immediately, their reliability as a partner comes into question.

WaaS will also be a more attractive option as the industry makes advancements in instrumentation and Ai to immediately detect and respond to changes in wastewater, as this creates complete transparency between the client and operator, and any problems can be addressed immediately.

Share this insight